Telematics insurance discounts: what UK fleets need to know

Many fleet operators assume that signing up for a telematics programme automatically unlocks significant premium savings. The reality of what is telematics insurance discount, and how it actually functions for commercial fleets, is considerably more nuanced. Some operators see meaningful reductions. Others see no change at all, or even watch premiums rise. Understanding the mechanics, realistic expectations, and the privacy trade-offs involved is what separates fleets that genuinely benefit from those that find the whole exercise disappointing.

Table of Contents

- Key takeaways

- What is a telematics insurance discount?

- Realistic savings and what affects them

- Privacy concerns and adoption barriers

- Getting the most from a telematics programme

- My honest take on telematics discounts

- How Fleetalyse supports your telematics insurance outcomes

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Discounts are not guaranteed | Telematics data can increase premiums for fleets with poor driving behaviour, not just reduce them. |

| Monitoring periods matter | Insurers typically collect driving data over around six months before adjusting premiums at renewal. |

| Telematics and NCD are separate | A telematics discount operates independently from your no-claims discount, affecting premiums through a different mechanism. |

| Privacy is a real barrier | Over 60% of UK drivers have concerns about sharing driving data, which affects driver buy-in across fleets. |

| Pilot before full rollout | Testing a telematics programme on a subset of vehicles first gives you baseline data to negotiate with insurers effectively. |

What is a telematics insurance discount?

A telematics insurance discount is a pricing benefit applied to your policy when you participate in a programme that monitors driving behaviour through onboard technology. The insurer uses data collected from your vehicles to assess actual risk, rather than relying purely on proxy factors like vehicle type, location, or driver age. If that data reflects low-risk driving, your premium is reduced accordingly.

The formal term used in the insurance industry is “usage-based insurance” (UBI), sometimes called “pay-how-you-drive” (PHYD) in commercial contexts. Telematics discount is the everyday shorthand, but knowing the industry terminology matters when you are negotiating with brokers or reviewing policy documentation.

How does telematics work in practice?

The monitoring is carried out through a telematics device fitted to each vehicle. In UK commercial fleets, this is typically a hardwired GPS unit, a plug-and-play OBD device, or increasingly, a smart dashcam with integrated telematics. These devices capture a range of data points continuously:

- Speed and acceleration patterns relative to posted limits and road conditions

- Braking behaviour, including instances of harsh or emergency braking

- Mileage covered, broken down by route and time period

- Time of day travel, since night driving and early morning motorway runs carry different risk profiles

- Cornering and lane discipline, where dashcam-integrated units provide additional context

This data feeds into a driver score or fleet score, which the insurer uses to calculate your premium adjustment. Driving behaviour data is typically collected over approximately six months before the score is finalised ahead of your policy renewal.

One distinction worth grasping clearly: a telematics discount and a no-claims discount are separate mechanisms. Your NCD accrues based on claims history. Your telematics discount is calculated from live behavioural data. You can have a strong NCD and still receive a poor telematics score if your drivers are speeding or braking harshly. Both affect your total premium, but through entirely different pathways.

Realistic savings and what affects them

The headline figures you will encounter when researching telematics insurance savings can look attractive. Some insurers advertise discounts of up to 30 to 40%. But those numbers represent the ceiling under ideal conditions, not the average outcome across a fleet.

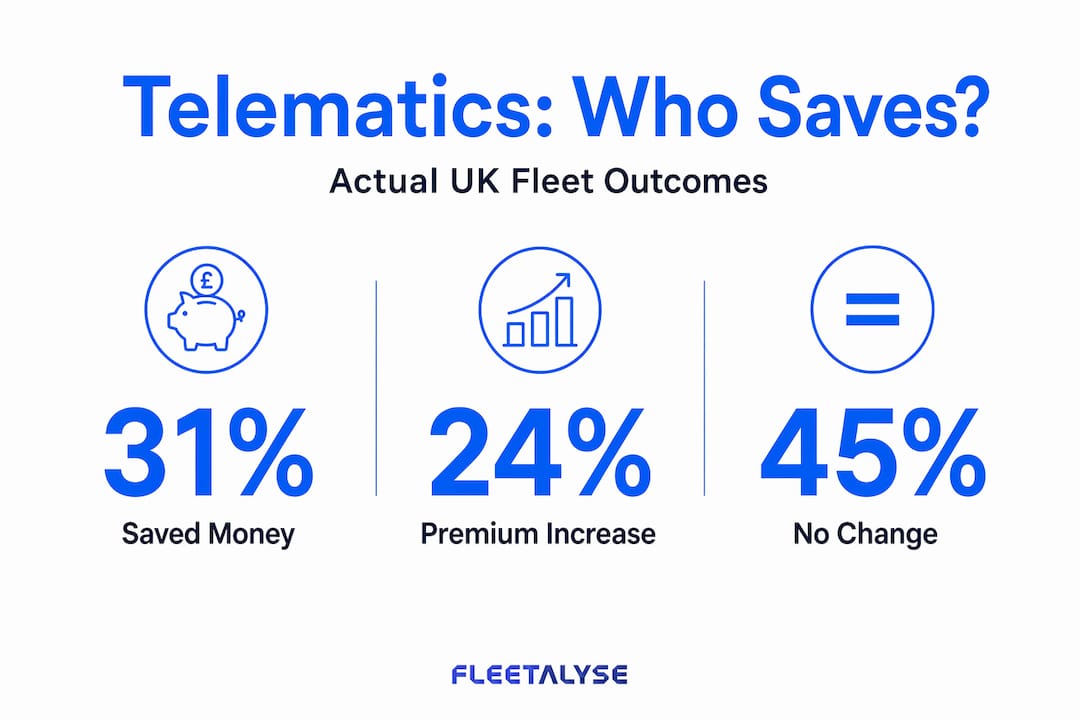

US market data from 2023 showed that only 31% of telematics enrolees actually saved money, while 24% saw their premiums rise and 45% saw no material change. The UK commercial fleet market has its own dynamics, but the variability is comparable. Commercial underwriting already accounts for many exposure factors before behavioural data is layered in, which means the telematics discount operates as an incremental adjustment rather than a wholesale repricing.

The table below summarises how typical driving behaviours map to discount outcomes:

| Driving behaviour | Likely premium impact |

|---|---|

| Consistent speed compliance, smooth braking | Premium reduction of 10 to 25% |

| Occasional harsh braking, minor speeding | Minimal change or small reduction |

| Frequent harsh braking, regular speeding | Premium increase or discount withdrawal |

| High mileage but low-risk behaviour | Modest reduction, mileage partially offsets gains |

| Late-night driving, high-risk routes | Neutral to negative impact, depending on insurer model |

Some insurers conduct mid-term reviews rather than waiting for renewal. If your fleet’s scores deteriorate significantly mid-policy, you may receive a premium increase notice before your renewal date. This is particularly relevant for larger fleets where driver turnover means consistent monitoring is a genuine operational challenge.

Pro Tip: Ask your insurer or broker specifically whether their telematics programme can impose a mid-term surcharge. Not all policies work this way, but assuming they do not and then receiving an unexpected increase mid-year creates real budget problems.

Some insurers also allow safer driving behaviour to be priced more fairly relative to actual risk rather than demographic proxies, which is one of the more compelling arguments for smaller fleets that have been categorically penalised by postcode or vehicle class in the past.

Privacy concerns and adoption barriers

Any honest assessment of the benefits of telematics insurance has to address the privacy question directly. 62% of UK respondents in a recent survey expressed concern about sharing their driving data with insurers, and only 19% had actually taken out a telematics policy. For fleet operators, this creates a practical problem: driver resistance can undermine the consistency of data needed to generate positive scores.

The specific concerns your drivers are likely to raise include:

- Data ownership and access. Who holds the driving data, for how long, and can it be used against a driver in a disciplinary or legal context outside of insurance purposes?

- Surveillance beyond working hours. Drivers who take vehicles home may feel uncomfortable with continuous location tracking during personal time.

- Score transparency. If a driver receives a poor score, they want to understand exactly which events caused it and have an opportunity to challenge inaccuracies.

- Third-party data sharing. Can the insurer sell or share behavioural data with other organisations, including employers beyond what the driver has consented to?

Fleet managers who dismiss these concerns tend to see lower compliance and poorer quality data. A more effective approach is to treat transparent data usage policies as a precondition for adoption, not an afterthought. This means issuing clear written policies to drivers that define what is collected, how it is used, who can access it, and what rights they have to query their scores.

From a legal standpoint, fleet operators processing driver data under a telematics programme must comply with UK GDPR. Drivers should receive a privacy notice specific to the telematics system, and any use of that data for employment-related decisions needs to be clearly scoped. This is not optional and, frankly, any insurer or telematics provider that cannot explain their data governance position clearly is a red flag.

Getting the most from a telematics programme

If you have weighed the options and concluded that telematics is worth it for your fleet, the difference between a modest saving and a meaningful one lies almost entirely in how you implement and manage the programme. Reactive adoption, where you simply fit devices and wait for renewal, tends to produce mediocre results. Proactive management produces better scores, better data, and better outcomes in premium negotiations.

Here is a structured approach that works in practice:

-

Pilot with a representative sample. Select 10 to 20% of your fleet across different routes, vehicle types, and drivers. Run the telematics programme for a full monitoring period and use the data to establish a baseline before committing the full fleet.

-

Set internal scoring targets aligned to insurer criteria. Ask your insurer what specific score thresholds determine discount eligibility. Build those targets into your internal KPIs and communicate them to drivers with context, not just directives.

-

Invest in active driver coaching. The most effective telematics programmes combine monitoring with coaching. A driver who understands why harsh braking scores negatively and receives feedback in near real time will improve faster than one who only finds out at renewal.

-

Use your telematics dashboard overview regularly. Weekly reviews of fleet-wide and individual scores let you intervene early rather than discovering problems at the end of a monitoring period.

-

Align your hardware with insurer requirements. Some insurers specify approved devices or data formats. Using a GPS vehicle tracker or smart dashcam that generates compatible data avoids disputes over data quality at renewal time.

-

Track the indirect effect on your NCD. While telematics scores and your no-claims discount are separate mechanisms, reduced claims frequency from improved driver behaviour will preserve and strengthen your NCD over time.

Pro Tip: Request a sample of your telematics data before renewal, not just a summary score. The underlying event log, including timestamps and GPS coordinates for scored incidents, gives you leverage to dispute outliers and negotiate more precisely with your insurer.

My honest take on telematics discounts

I’ve worked with enough UK fleet operators to know that telematics insurance is genuinely useful but genuinely misunderstood. The question I hear most often is whether telematics is worth it, and my answer is always the same: it depends on what you do with the data.

What I’ve found consistently is that fleets chasing the discount figure alone rarely achieve it. The ones that benefit most treat telematics as a risk management tool first and an insurance pricing mechanism second. When your drivers’ scores improve because you’ve built a culture of accountability and coaching, the insurance saving follows. When you simply install devices and hope for the best, you often end up in that 45% that sees no material change.

I’ve also seen fleets make the mistake of promising drivers that telematics will definitely reduce the business’s insurance costs, then losing credibility when it does not. Undersell the potential discount and oversell the safety benefits. That framing holds up regardless of what the renewal quote looks like.

The privacy conversation is one I’d encourage every fleet manager to have openly, before fitting a single device. Drivers who feel informed and respected are far more likely to modify their behaviour in a way that generates good scores. Resentful compliance produces inconsistent data and no improvement in actual risk.

Finally, watch how the technology evolves. AI-powered dashcams are beginning to generate richer contextual data than simple GPS and accelerometer units. Within two to three years, underwriters who use this data will likely be able to price commercial fleet risk with considerably more precision. Getting comfortable with telematics now positions your fleet well for that shift.

— Vytautas

How Fleetalyse supports your telematics insurance outcomes

If you are evaluating telematics as part of a broader effort to control fleet costs and improve safety, having the right hardware and data infrastructure makes a material difference to the quality of your insurance case. Fleetalyse provides UK fleet operators with GPS tracking and smart dashcam solutions designed to generate the kind of consistent, high-quality behavioural data that insurers actually want to see.

The Fleetalyse platform gives you real-time visibility into driver behaviour across your entire fleet, whether you operate cars, vans, HGVs, or trailers. The telematics solutions include driver scoring, route analysis, and fuel consumption monitoring, all accessible through a single dashboard. For fleets running heavy goods vehicles, HGV GPS trackers with tachograph integration mean your compliance data and insurance-relevant behavioural data sit in one place, reducing administrative workload while strengthening your position at renewal.

Fleetalyse’s UK-based support team can help you configure monitoring parameters aligned to your insurer’s criteria, giving your programme the best possible chance of generating meaningful telematics insurance savings from day one.

FAQ

What is a telematics insurance discount?

A telematics insurance discount is a premium reduction offered by insurers to policyholders who share driving behaviour data collected through onboard devices. Discounts are applied at renewal based on scores derived from speed, braking, mileage, and other behavioural metrics.

How much can a UK fleet save with telematics insurance?

Savings vary considerably. Insurers advertise discounts of up to 30 to 40%, but actual outcomes differ widely, with a significant proportion of enrolees seeing no change or premium increases depending on fleet driving behaviour and insurer methodology.

Does a telematics discount affect my no-claims discount?

No, they are separate mechanisms. A telematics discount is calculated from behavioural data, while your no-claims discount accrues from claims history. However, improved driving behaviour can reduce claims frequency, which indirectly protects and strengthens your NCD over time.

Why are UK drivers reluctant to use telematics insurance?

Privacy concerns are the primary barrier, with 62% of UK respondents worried about how their driving data is used and shared. Transparency from both insurers and fleet managers is the most effective way to address this.

What devices are used for telematics in UK commercial fleets?

UK fleets typically use hardwired GPS trackers, plug-and-play OBD units, or smart AI dashcams with integrated telematics capabilities. The right device depends on your vehicle types, insurer requirements, and whether you also need compliance data such as tachograph records.